Source: Factset

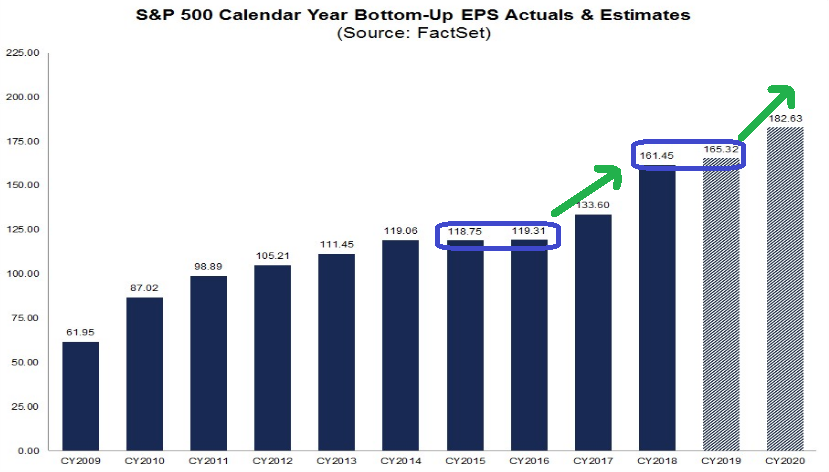

As we’ve stated in previous posts (under category “Earnings”), 2020 earnings are setting up in a similar fashion to 2017. After a sideways period of flat market earnings and limited stock market appreciation from 2015-2016, earnings jumped in 2017. The market began to discount this earnings jump in late Q3 early Q4 2016 (end of first blue box below).

Earnings and stock market performance have similarly been flat for 2018-2019 setting up for a jump in 2020. With the discount rate coming down another 25-50bps before year end (with 1-2 more cuts), we will not only get the benefit of pricing forward earnings growth, but likely the new discount rate will afford reasonable multiple expansion.

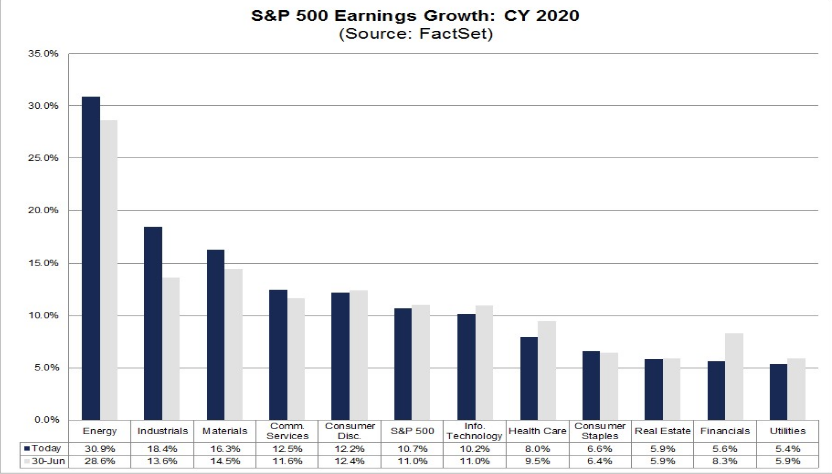

So where will this earnings growth come from? Energy, Industrials and Materials have the highest yoy growth expectations for 2020. The implication is a sector rotation in which the laggards of 2019 could potentially be amongst the leaders in 2020.