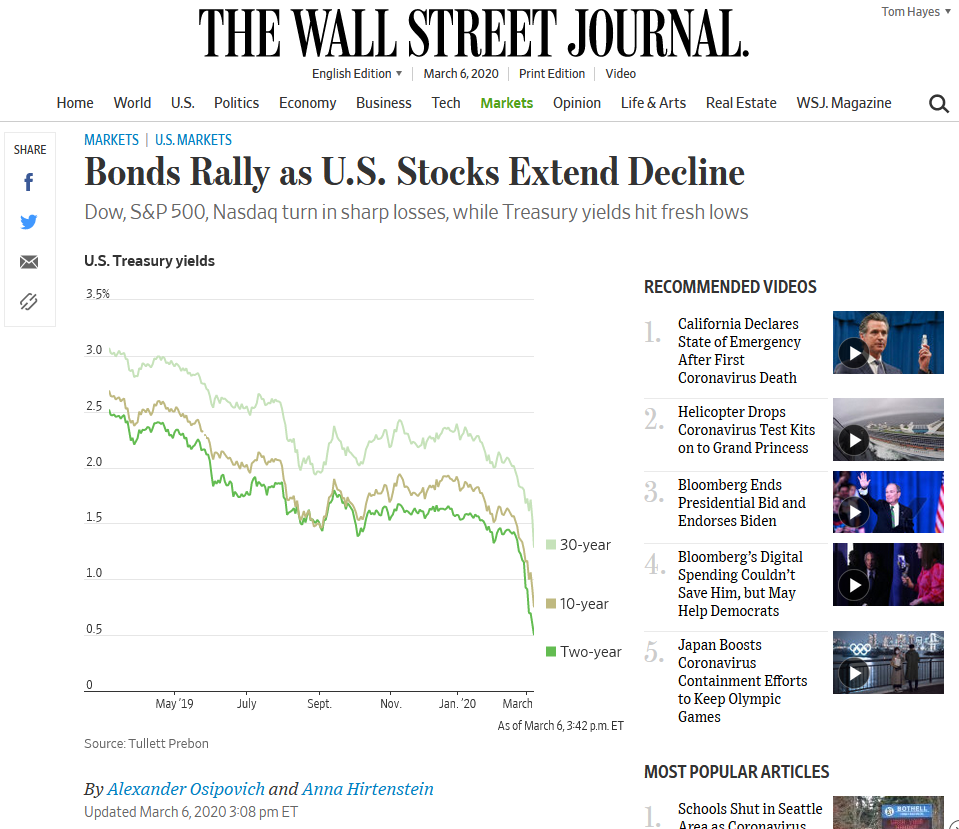

Thanks to Alexander Osipovich for including me in his and Anna Hirtenstein’s article in the The Wall Street Journal today:

“Investors continued to pile into safe-haven assets Friday, pushing the yield on long-term U.S. government bonds to unprecedented levels.” You can read it here:

Click Here to View The Full Article at The Wall Street Journal