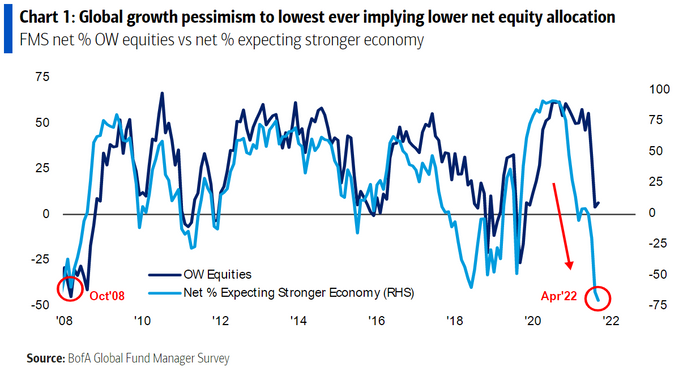

The April 1-7 survey covered 292 managers with $833 Billion in assets under management. Continue reading “April 2022 Bank of America Global Fund Manager Survey Results (Summary)”

Category: Sentiment

The “Shake it Off” Stock Market (and Sentiment Results)…

On August 19, 2014, Taylor Swift released her hit song “Shake it Off.” It was nominated for three Grammy awards in 2015 and named one of the 10 songs that defined the 2010’s by USA Today. The key lyrics that relate to the current state of the stock market are as follows: Continue reading “The “Shake it Off” Stock Market (and Sentiment Results)…”

To Invert or Not To Invert? That is the key Stock Market question…

On Tuesday, the 2/10 yield curve inverted by -3bps (for a few minutes) and closed with a positive spread +2bps on the day. There are a number of factors that led to this incident, but one stands out from the crowd. Continue reading “To Invert or Not To Invert? That is the key Stock Market question…”

Avoid the Noid – Stock Market (and Sentiment Results)…

Wikipedia, “The Noid was an advertising character for Domino’s Pizza created in the 1980s. Clad in a red, skin-tight, rabbit-eared body suit with a black N inscribed in a white circle on his chest, the Noid was a physical manifestation of all the challenges inherent in getting a pizza delivered in 30 minutes or less. Though persistent, his efforts were repeatedly thwarted.”

Continue reading “Avoid the Noid – Stock Market (and Sentiment Results)…”

“Home Sweet Home” Stock Market (and Sentiment Results)…

In 1985 Motley Crue released one of its major all-time hits, “Home Sweet Home.” Last night, when I was thinking about the journey of Alibaba over the last few months, this song came to mind. The journey has had a few detours, but now it’s on finally on its way back “home” to intrinsic value.

Seeing Alibaba jump ~35% in one day is evidence that the objective business/fundamental analysis was always accurate, it was simply a mercurial government leadership holding the stock back. With the government now stepping out of the way and letting business flourish once again, we expect this marvelous business to work its way back to intrinsic value over time. We may hit a few more potholes and speed bumps, but we’re on our way… Continue reading ““Home Sweet Home” Stock Market (and Sentiment Results)…”

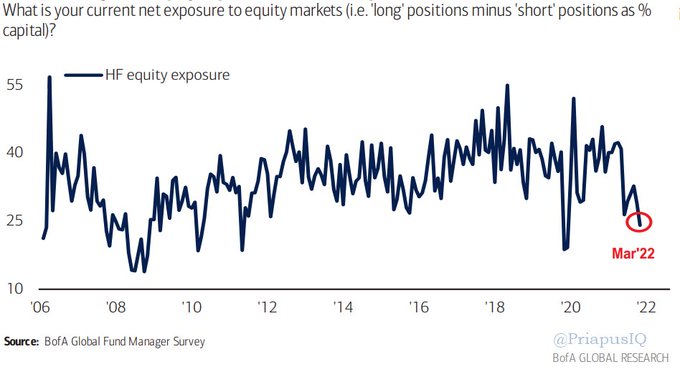

March 2022 Bank of America Global Fund Manager Survey Results (Summary)

The March 4-10 survey covered 341 managers with $1 trillion in assets under management. Continue reading “March 2022 Bank of America Global Fund Manager Survey Results (Summary)”

The “Horseshoes and Hand Grenades” Stock Market (and Sentiment Results)…

While it looks like we are finally close to the inflection we discussed last week, we must vigilantly recognize the salient lyrics in Country Star Mitchell Tenpenny’s new hit: Continue reading “The “Horseshoes and Hand Grenades” Stock Market (and Sentiment Results)…”

The Stock Market Bet You Can’t Collect On…

On Wednesday morning I joined Alicia Nieves on Cheddar’s “Opening Bell.” Thanks to Alicia, Ally Thompson and Jovan Collins for having me on:

Continue reading “The Stock Market Bet You Can’t Collect On…”

The Stock Market’s Biggest Risk…

Rudyard Kipling, “If you can keep your head when all about you are losing theirs… Yours is the Earth and everything that’s in it, And—which is more—you’ll be a Man, my son!” Continue reading “The Stock Market’s Biggest Risk…”

Backward Looking Allocators, Forward Looking Opportunities…

On Wednesday afternoon (after the Fed Minutes were released), I joined Liz Claman on Fox Business – The Claman Countdown – to discuss the Stock Market, the Fed, and Russia. Thanks to Liz and Ellie Terrett for having me on: Continue reading “Backward Looking Allocators, Forward Looking Opportunities…”