For the past six weeks every movement of the stock market has been predicated on what the Fed had to say about their future outlook/actions. Tomorrow we start earnings season in earnest with reports from the Big Banks (JPM, WFC, C, MS). Early this morning I was on CNBC Closing Bell (Indonesia) to discuss the setup going into earnings.

We are in a very similar situation to the setup in June when analysts were calling for a 20% reduction in earnings estimates and misses across the board. Not only did estimates hold up better than expected, but earnings materially beat expectations – fueling a ~20% rally over 8 weeks, until the Fed began a panicked hawkish jawboning campaign to attempt to destroy demand and anchor longer run inflation expectations.

We covered a lot of new ground in this extended interview which will be helpful in understanding the setup/expectations and outcomes for earnings season. Thanks to Andi Shalini and Yudha Yudistira for having me on Closing Bell. Watch it here:

Credit

This is the most important chart I am watching. It is high yield credit spreads. It is our view that the current credit disruption is an aftershock from 2020 (like 2018, 2011, 2005) and not the beginning of a new earthquake (2020, 2009, 2002):

As we discussed in the CNBC interview above, the Fed will be forced to relent when government, municipalities, households and businesses can’t refinance. The cost of not intervening will be much higher (economic crisis bailout) than the cost of running inflation above trend for several years – as we did post-WWII when Debt/GDP also exceeded 120%. Whether it’s a Draghi “whatever it takes” moment like 2011 or a Mnuchin “backstop the corporate credit markets” in 2020, when credit markets freeze, policy makers bend. The hawkish talk works – until it doesn’t.

As we discussed in the CNBC interview above, the Fed will be forced to relent when government, municipalities, households and businesses can’t refinance. The cost of not intervening will be much higher (economic crisis bailout) than the cost of running inflation above trend for several years – as we did post-WWII when Debt/GDP also exceeded 120%. Whether it’s a Draghi “whatever it takes” moment like 2011 or a Mnuchin “backstop the corporate credit markets” in 2020, when credit markets freeze, policy makers bend. The hawkish talk works – until it doesn’t.

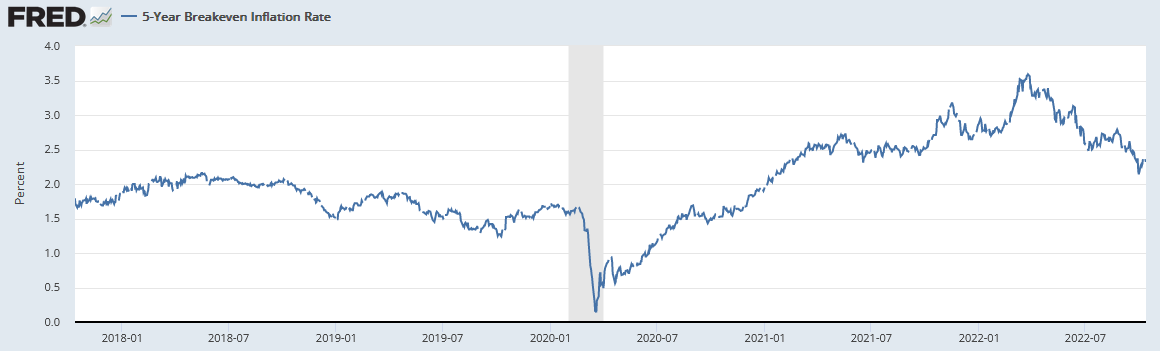

So far, the ECB has had to relent with their new QE facility to buy Italian bonds, the Bank of England has had to relent by buying Gilts to bail out UK pensions, and the RBA hiked rates less than expected in Australia at their last meeting. The only way to lower global debt to sustainable levels is to let inflation run above trend for the next 3-5 years as they did following WWII. This time will be no different. But the “TALK” (not action) must remain tough/hawkish the whole way through to ensure Long-Term inflation expectations remain anchored. So far the tough talk is working:

Fed Minutes Review

Below I have highlighted the key points from the Fed Minutes released yesterday:

Developments in Financial Markets and Open Market Operations

The market-implied path suggested reasonable odds of additional 75 basis point and 50 basis point rate increases at the November and December meetings, respectively. Market participants generally anticipated a further slowing in the pace of rate increases after December, with the peak policy rate being reached in the first half of 2023.

Balance sheet runoff had continued to proceed smoothly over the intermeeting period. With caps on redemptions of Treasury securities and agency mortgage-backed securities (MBS) doubling in September, the pace of balance sheet runoff was set to increase over coming months. The markets for Treasury securities and agency MBS continued to function in an orderly manner, though liquidity conditions in both markets remained low, reflecting elevated interest rate uncertainty.

Staff Review of the Economic Situation

The information available at the time of the September 20–21 meeting suggested that U.S. real GDP was increasing at a modest pace in the third quarter after having declined over the first half of the year.

Staff Review of the Financial Situation

Measures of current loan performance for businesses and most households remained generally stable. However, more recently, expectations of future credit quality for businesses deteriorated slightly, and delinquency rates rose for some types of credit owed by households with low credit scores.

Corporate bond spreads narrowed slightly, on net, and remained roughly at the midpoints of their historical distributions. Reflecting increases in both policy rates and corporate bond spreads, yields on corporate bonds rose significantly since the start of the year. Municipal bond spreads over comparable-maturity Treasury yields widened a touch.

In domestic credit markets, borrowing costs continued to rise over the intermeeting period. Yields on both corporate bonds and institutional leveraged loans increased. Bank interest rates for commercial and industrial (C&I) and commercial real estate (CRE) loans also increased. Among small businesses that borrow on a regular basis, the share of firms facing higher borrowing costs continued to climb through August. Municipal bond yields increased across ratings categories. Borrowing costs for residential mortgage loans increased and reached their highest levels since 2008. Interest rates on most credit card accounts continued to move higher, in line with the rise in the federal funds rate, and auto loan interest rates rose steadily through August.

Credit remained generally available to businesses and households, but high borrowing costs appeared to reduce the demand for credit, resulting in lower financing volumes in some markets. Issuance of nonfinancial corporate bonds slowed further in July from the weak levels seen in the second quarter but rebounded somewhat in August and so far in September. Gross institutional leveraged loan issuance increased modestly in July from subdued levels but continued to be weak in August. Equity issuance remained depressed, while issuance of municipal bonds was sluggish over the summer and so far in September.

The share of small firms reporting that it was more difficult to obtain loans continued its upward trend in August but remained lower than its historical average.

The credit quality of nonfinancial corporations remained generally strong, with low default rates for both corporate bonds and leveraged loans. The volume of rating upgrades in the corporate bond market outpaced that of downgrades in July and August, but, so far in September, these relative volumes reversed. The volume of rating downgrades in the leveraged loan market continued to exceed that of upgrades.

Staff Economic Outlook

On a 12-month change basis, total PCE price inflation was expected to be 5.1 percent in 2022, and core inflation was expected to be 4.3 percent. Although the staff continued to project that core inflation would step down over the next two years—reflecting the anticipated resolution of supply–demand imbalances and a labor market that was expected to become less tight—core inflation was revised up in each year of the projection. In 2025, core inflation was expected to be 2.1 percent. Total PCE price inflation was expected to decline to 2.6 percent in 2023 as core inflation slowed and energy prices declined. Total PCE inflation was expected to move down further in 2024, to 2 percent, and to remain at 2 percent in 2025.

Participants’ Views on Current Conditions and the Economic Outlook

Participants revised down their projections of real GDP growth for this year from their projections in June. Several participants noted that the continued strength in the labor market, as well as the data on gross domestic income, raised the possibility that the current GDP data could understate the strength in economic activity this year. Participants generally anticipated that the U.S. economy would grow at a below-trend pace in this and the coming few years, with the labor market becoming less tight, as monetary policy assumed a restrictive stance and global headwinds persisted. Participants noted that a period of below-trend real GDP growth would help reduce inflationary pressures and set the stage for the sustained achievement of the Committee’s objectives of maximum employment and price stability.

In their discussion of the household sector, participants noted that consumer spending grew moderately, reflecting strength in the labor market, the elevated level of household savings accumulated during the pandemic, and a strong aggregate household-sector balance sheet. Several participants noted that spending appeared to have held up relatively well, especially among higher-income households. These participants also noted that the composition of spending by low-to-moderate-income households—who were affected to a greater degree by high food, energy, and shelter prices—was changing, with discretionary expenditures being cut and purchases shifting to lower-cost options.

Participants anticipated that the supply and demand imbalances in the labor market would gradually diminish and the unemployment rate would likely rise somewhat, importantly reflecting the effects of tighter monetary policy. Participants judged that a softening in the labor market would be needed to ease upward pressures on wages and prices. Participants expected that the transition toward a softer labor market would be accompanied by an increase in the unemployment rate. Several commented that they considered it likely that the transition would occur primarily through reduced job vacancies and slower job creation.

With respect to the medium term, participants judged that inflation pressures would gradually recede in coming years. Various factors were cited as likely to contribute to this outcome, including the Committee’s tightening of its policy stance, a gradual easing of supply and demand imbalances in labor and product markets, and the likelihood that weaker consumer demand would result in a reduction of business profit margins from their current elevated levels. A few participants reported that business contacts in certain retail sectors—such as used cars and apparel—were planning to cut prices in order to help reduce their inventories.

In assessing inflation expectations, participants noted that longer-term expectations appeared to remain well anchored, as reflected in a broad range of surveys of households, businesses, and forecasters as well as measures obtained from financial markets. Participants remarked that the Committee’s affirmation of its strong commitment to its price-stability objective, together with its forceful policy actions, had likely helped keep longer-run inflation expectations anchored.

Participants broadly judged the risks to real GDP growth to be weighted to the downside, with various global headwinds most prominently cited as contributing factors.

Participants judged that the pace and extent of policy rate increases would continue to depend on the implications of incoming information for the outlook for economic activity and inflation and on risks to the outlook. Several participants noted that, particularly in the current highly uncertain global economic and financial environment, it would be important to calibrate the pace of further policy tightening with the aim of mitigating the risk of significant adverse effects on the economic outlook. Participants observed that, as the stance of monetary policy tightened further, it would become appropriate at some point to slow the pace of policy rate increases while assessing the effects of cumulative policy adjustments on economic activity and inflation. Many participants indicated that, once the policy rate had reached a sufficiently restrictive level, it likely would be appropriate to maintain that level for some time until there was compelling evidence that inflation was on course to return to the 2 percent objective. Participants noted that, in keeping with the Committee’s Plans for Reducing the Size of the Federal Reserve’s Balance Sheet, balance sheet runoff had moved up to its maximum planned pace in September and would continue at that pace. They further observed that a significant reduction in the Committee’s holdings of securities was in progress and that this process was contributing to the move to a restrictive policy stance.

Several participants observed that as policy moved into restrictive territory, risks would become more two-sided, reflecting the emergence of the downside risk that the cumulative restraint in aggregate demand would exceed what was required to bring inflation back to 2 percent. A few of these participants noted that this possibility was heightened by factors beyond the Committee’s actions, including the tightening of monetary policy stances abroad and the weakening global economic outlook, that were also likely to restrain domestic economic activity in the period ahead.

Committee Policy Action

Members agreed that, in assessing the appropriate stance of monetary policy, they would continue to monitor the implications of incoming information for the economic outlook and that they would be prepared to adjust the stance of monetary policy as appropriate if risks emerged that could impede the attainment of the Committee’s goals. They also noted that their assessments would take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

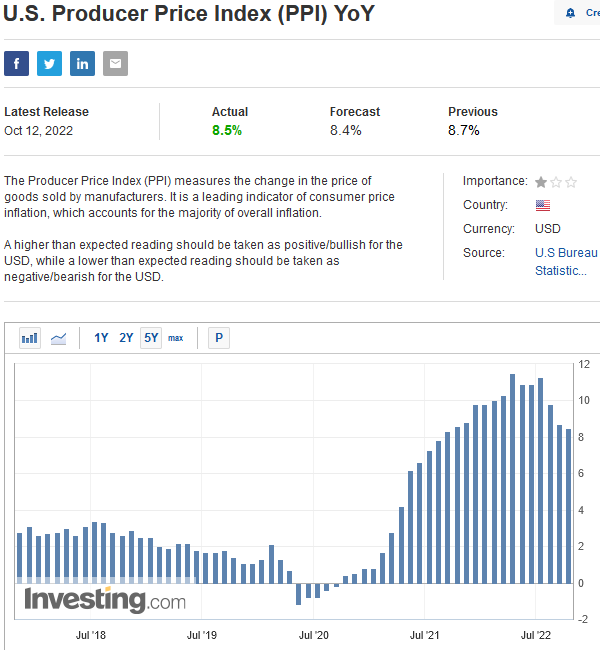

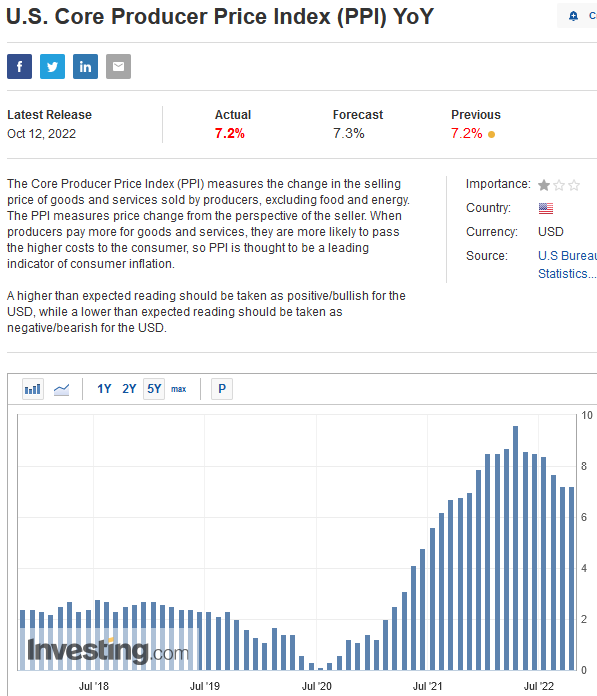

PPI – Producer Price Index

Right direction, wrong pace:

Now onto the shorter term view for the General Market:

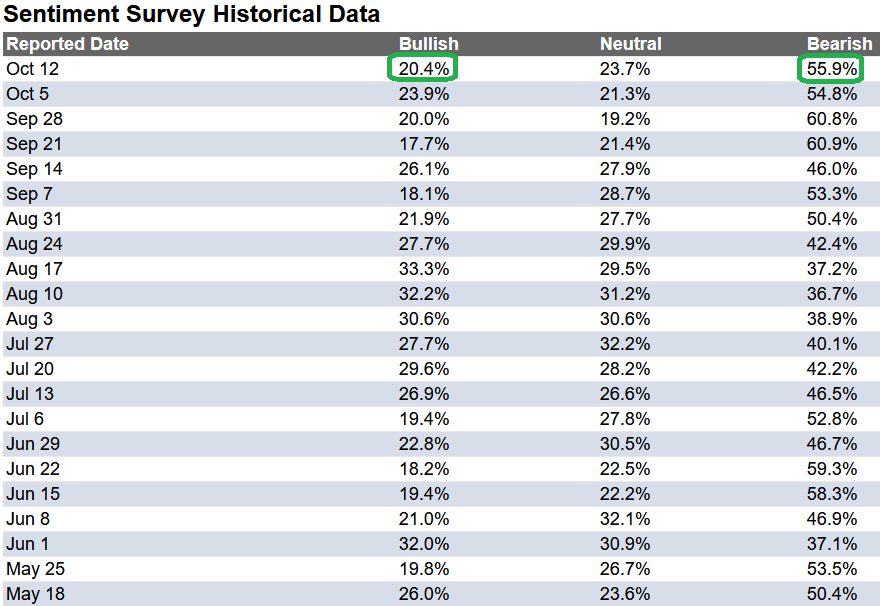

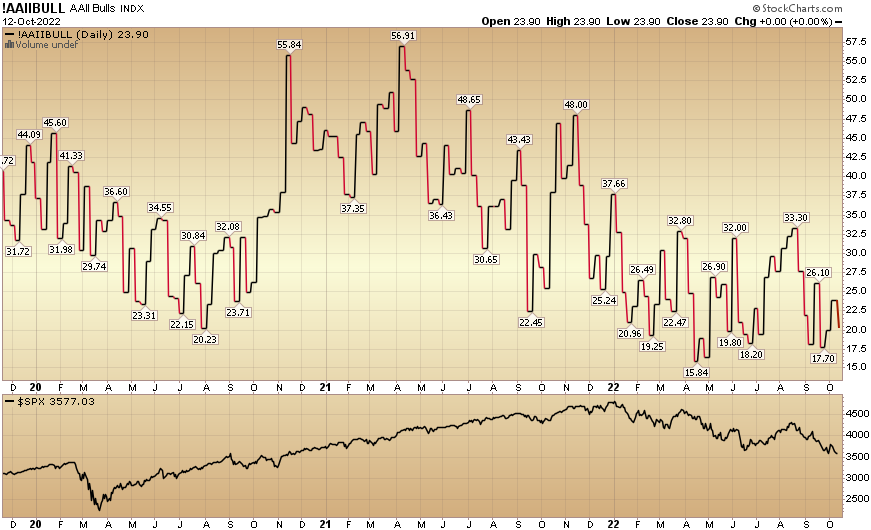

In this last week’s AAII Sentiment Survey result, Bullish Percent (Video Explanation) dropped to 20.4% from 23.9% the previous week. Bearish Percent ticked up to 55.9% from 54.8%. Retail Sentiment is at the levels it was at the pandemic lows (20.23) and near the Great Financial Crisis lows of (18.92).

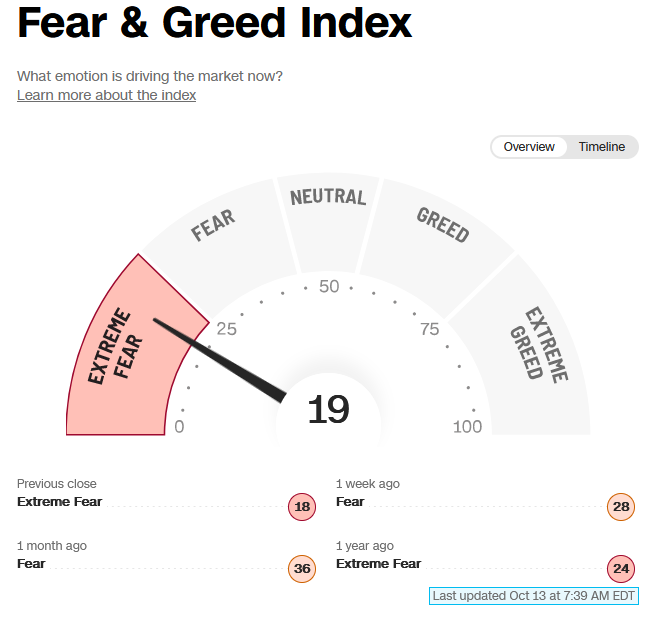

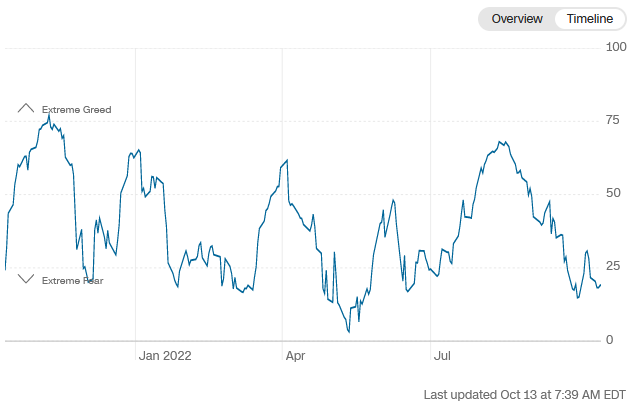

The CNN “Fear and Greed” flat-lined from 19 last week to 19 this week. Sentiment is still fearful. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The CNN “Fear and Greed” flat-lined from 19 last week to 19 this week. Sentiment is still fearful. You can learn how this indicator is calculated and how it works here: (Video Explanation)

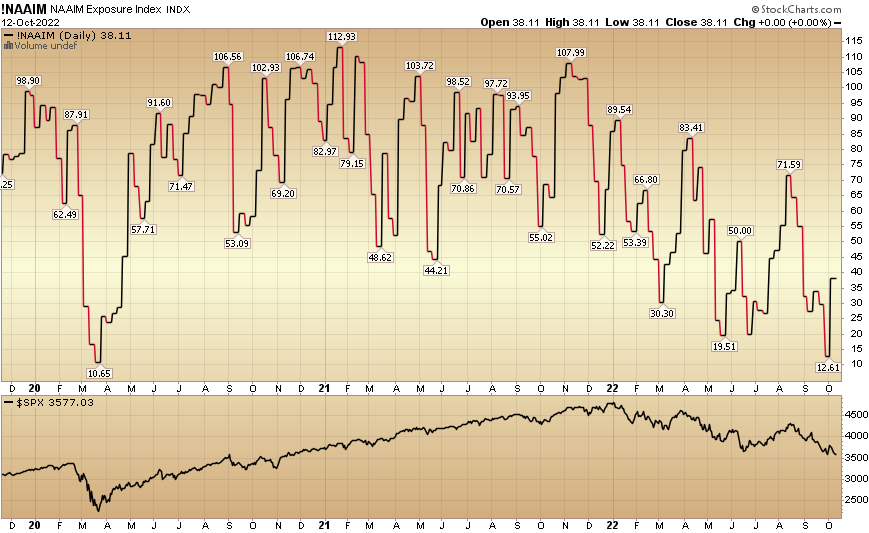

And finally, the NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 38.11% this week from 12.61% equity exposure last week.

Our podcast|videocast will be out on Friday this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.