Key Market Outlook(s) and Pick(s)

On Tuesday, I joined Karina Mitchell on CGTN America to discuss markets, outlook, tariffs, and where we see opportunities. Thanks to Karina and Bruno Felberg for having me on:

QXO Update

After a few months of back-and-forth negotiations, QXO and Beacon Roofing ($BECN) finally agreed on a $124.35-per-share cash deal worth ~$11 billion.

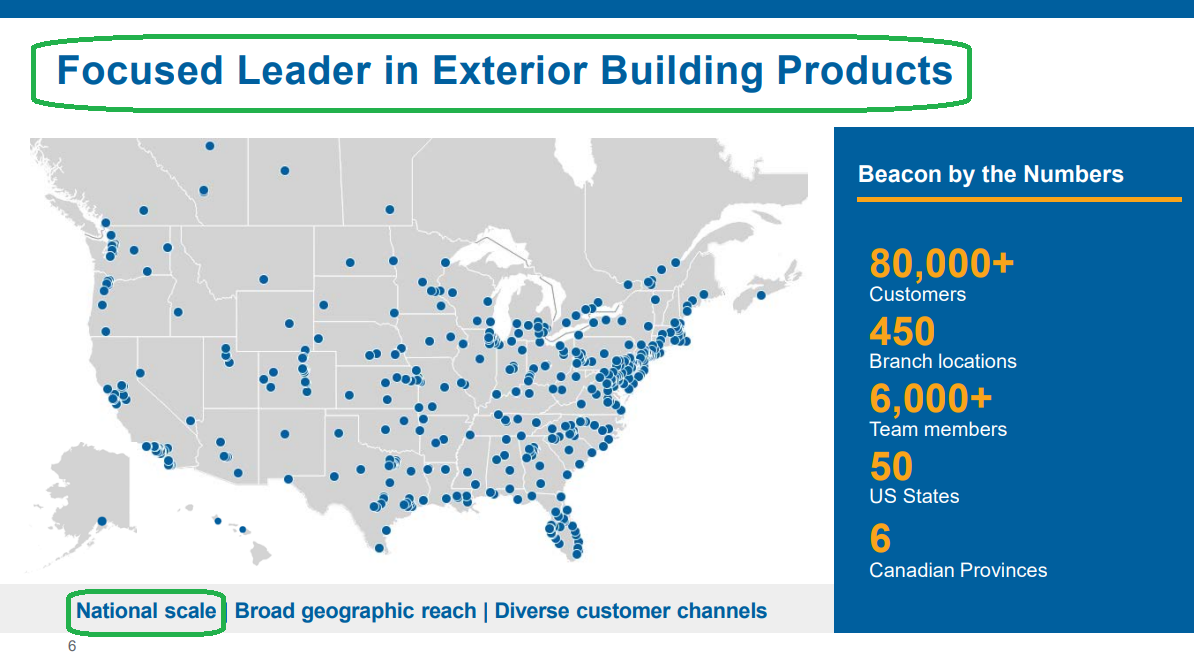

It’s easy to see why Brad Jacobs had his eyes set on Beacon. Beacon is the No. 2 player in the building products distribution space, an industry that has compounded at a 7% clip over the last five years. More importantly, it gives him the platform to start building QXO into the $50B+ powerhouse he has in mind. The opportunity was so attractive that he was willing to pay up for Beacon—something he doesn’t do often—offering a 40% premium over Beacon’s pre-acquisition price and paying ~10.5x EBITDA. If Jacobs delivers on his plan to double EBITDA in the next few years (and let’s face it, betting against him has never worked out well), the price tag could end up looking more like 5x EBITDA.

History doesn’t repeat, but it often rhymes…

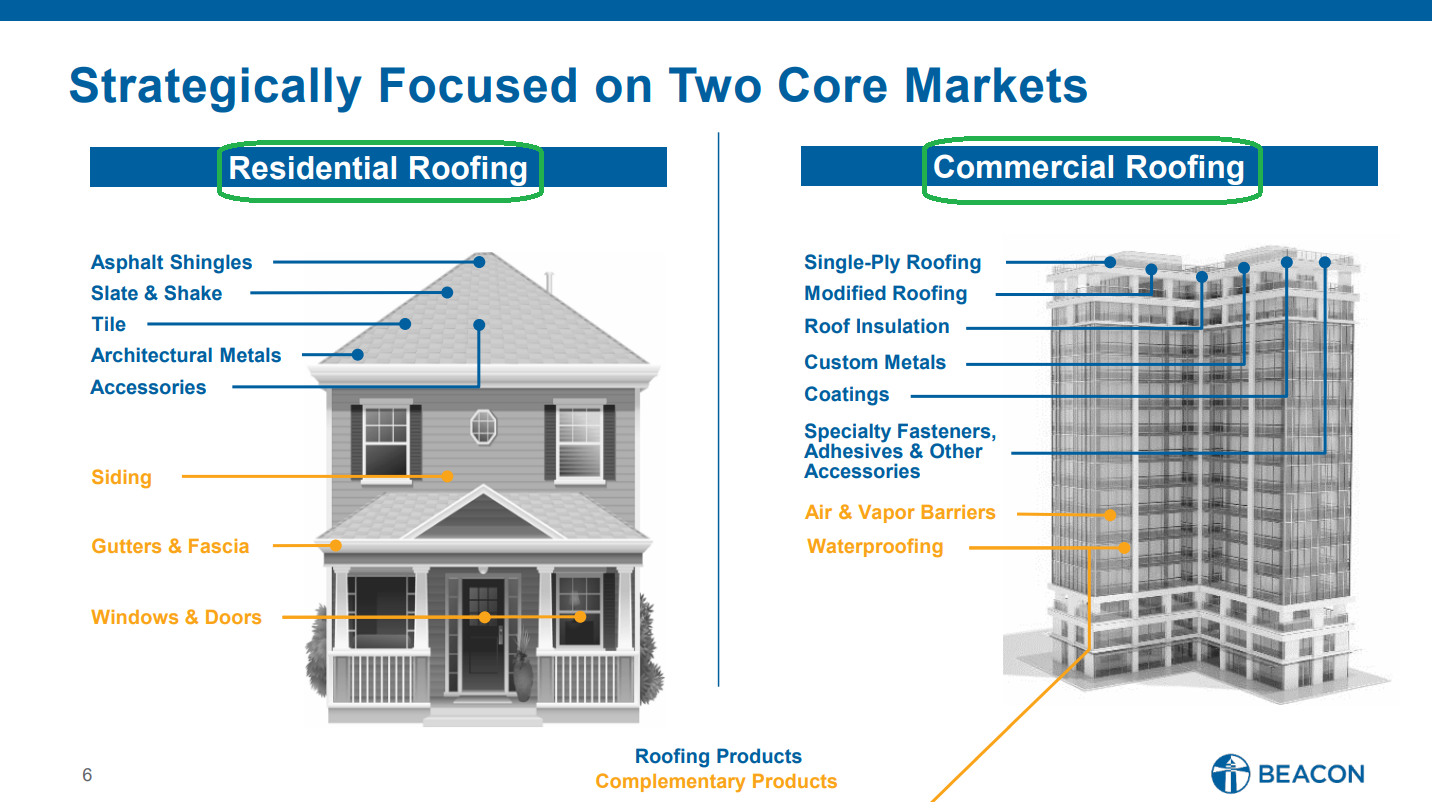

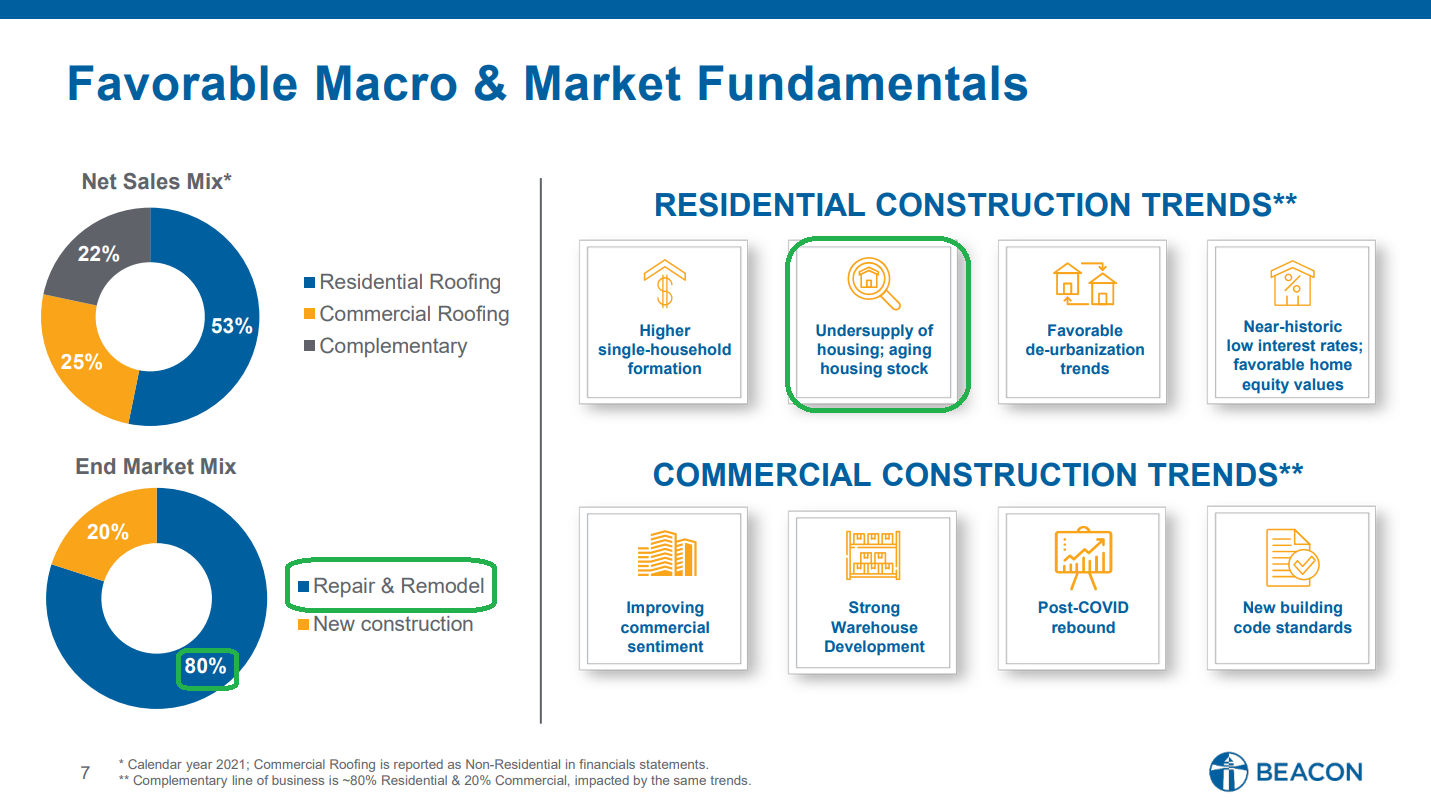

Part of what makes Beacon so attractive is that ~80% of its business comes from repair and remodeling, which is non-discretionary and far less cyclical. When your roof starts leaking, there’s no putting it off. Plus, with 97% of Beacon’s business being U.S.-based and domestically sourced, it’s practically immune to any tariff risk.

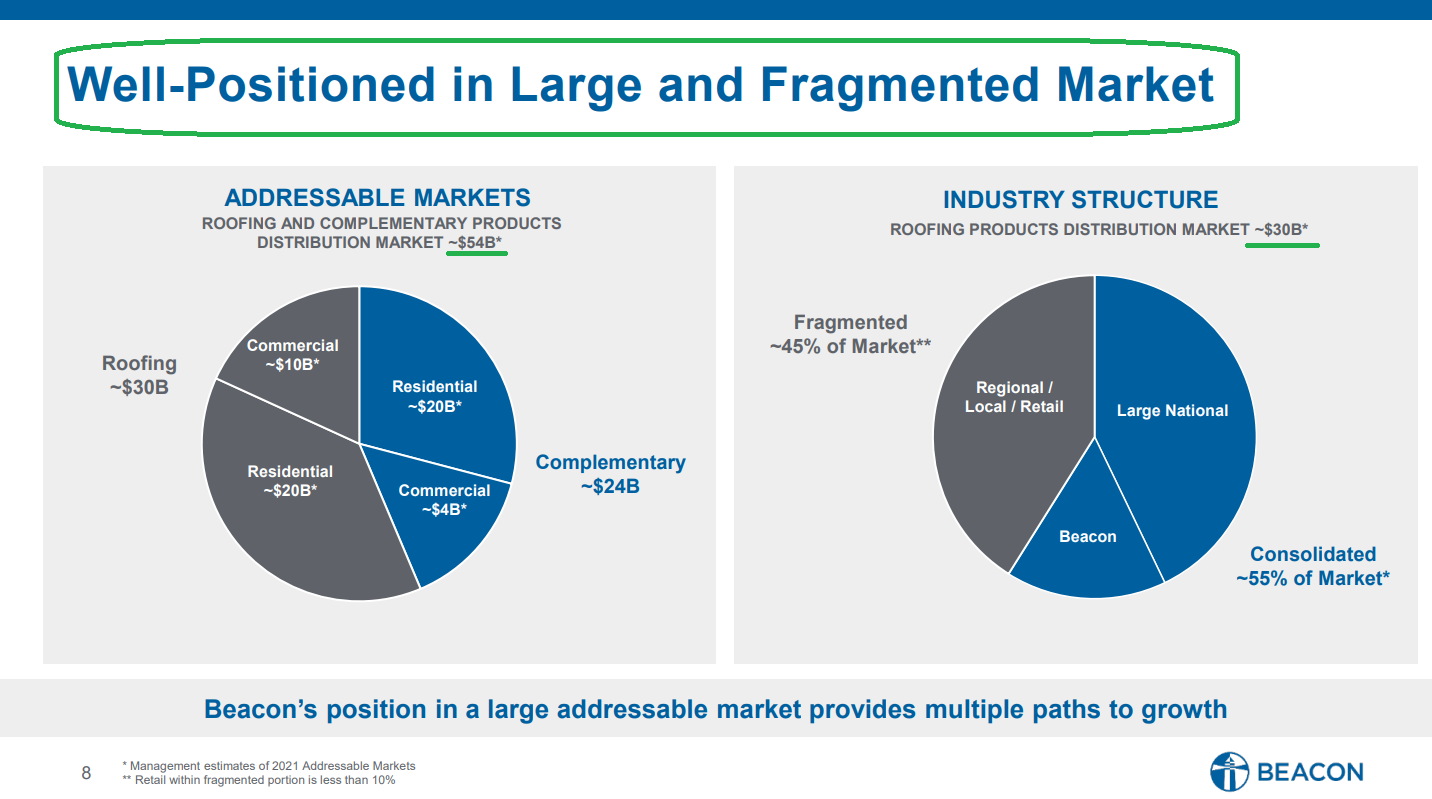

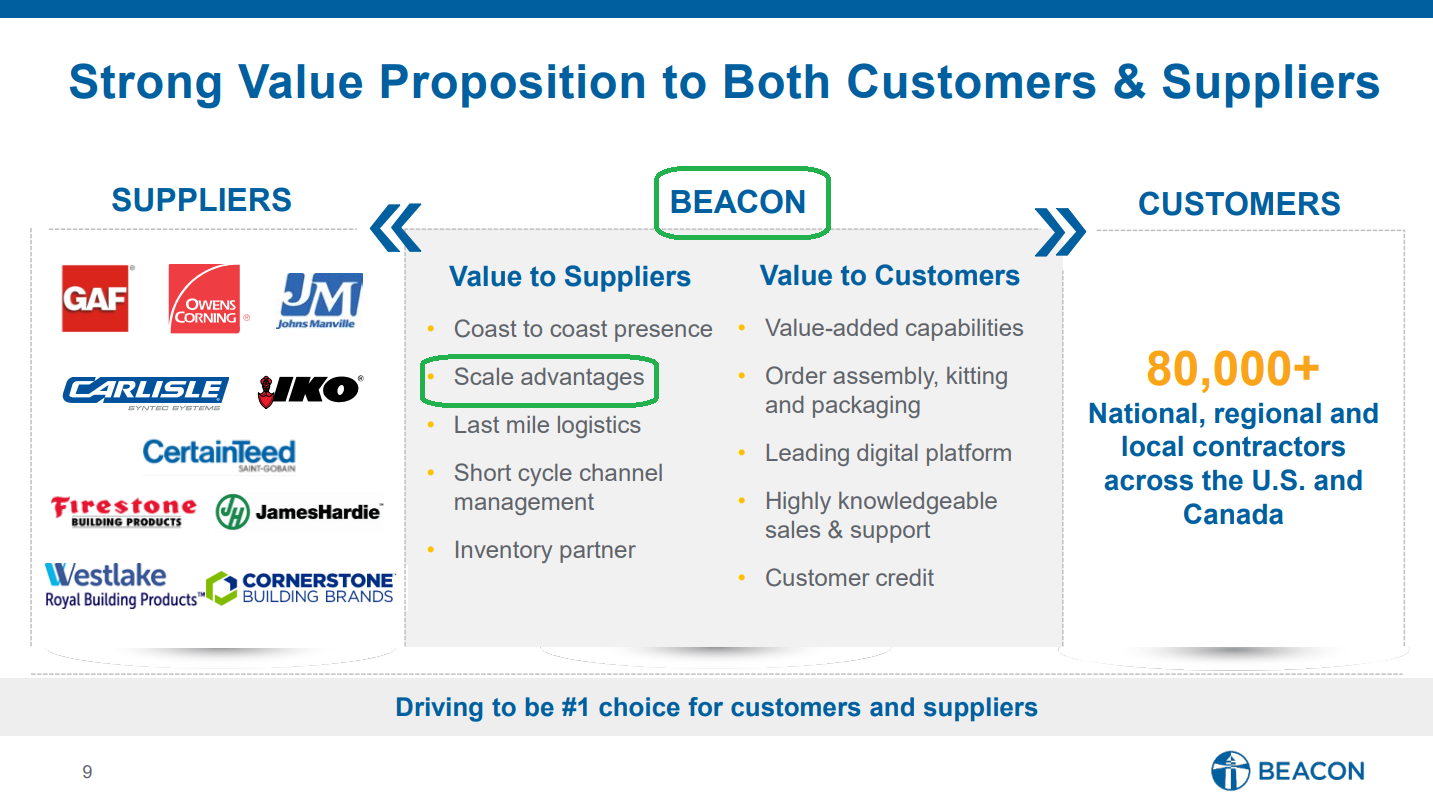

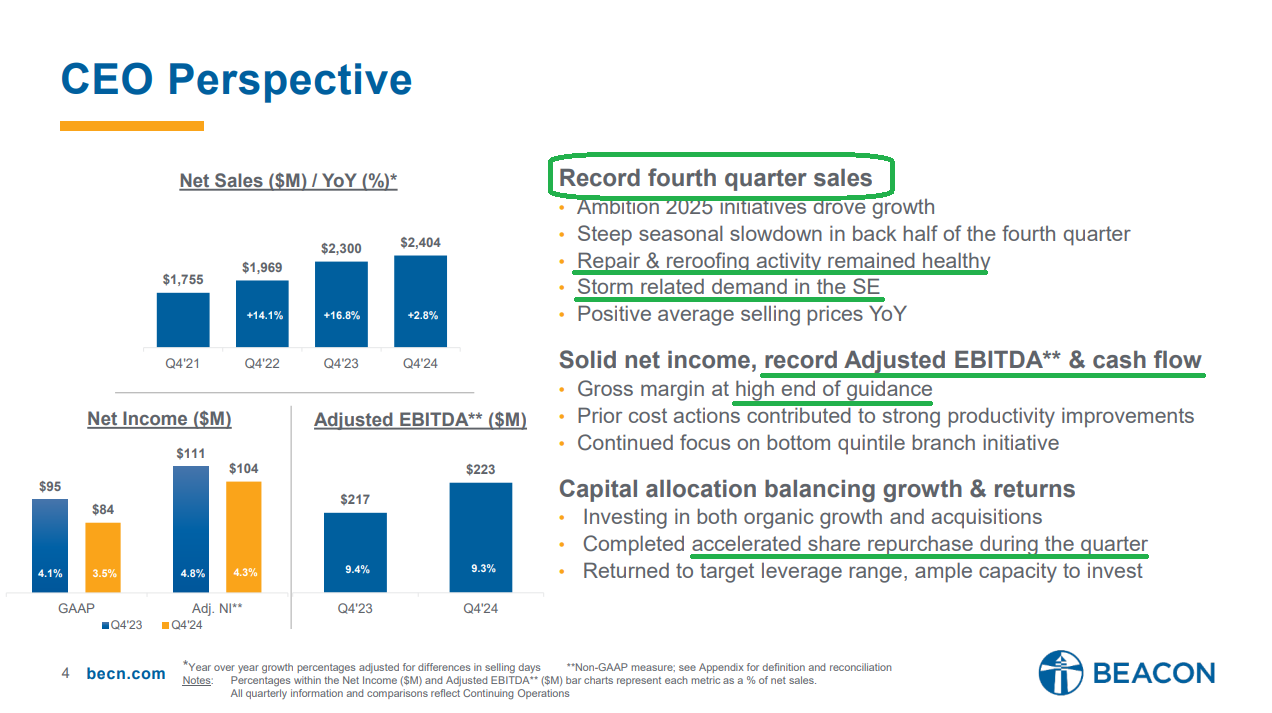

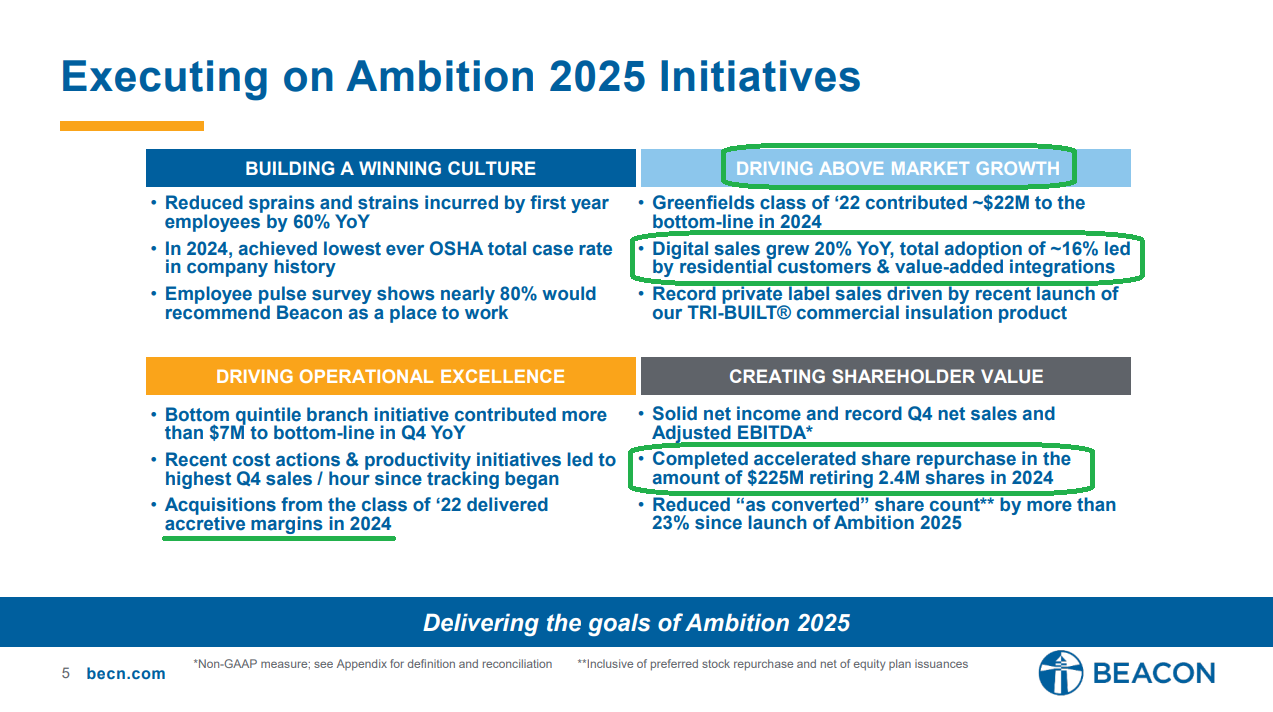

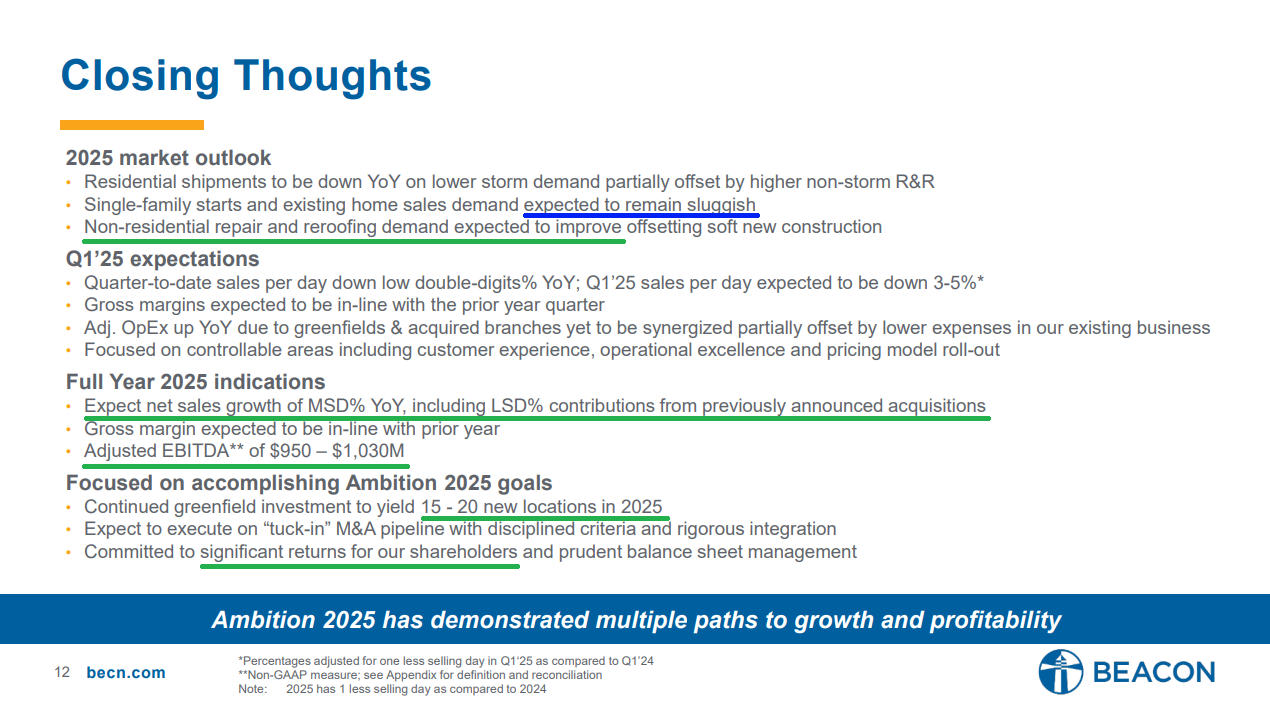

Here’s a bit more background on Beacon and its latest quarter:

This past week, Brad Jacobs went on the Bloomberg “Odd Lots” Podcast to discuss the deal, his plans for improving Beacon, and opportunities for QXO. I highly recommend giving it a listen below:

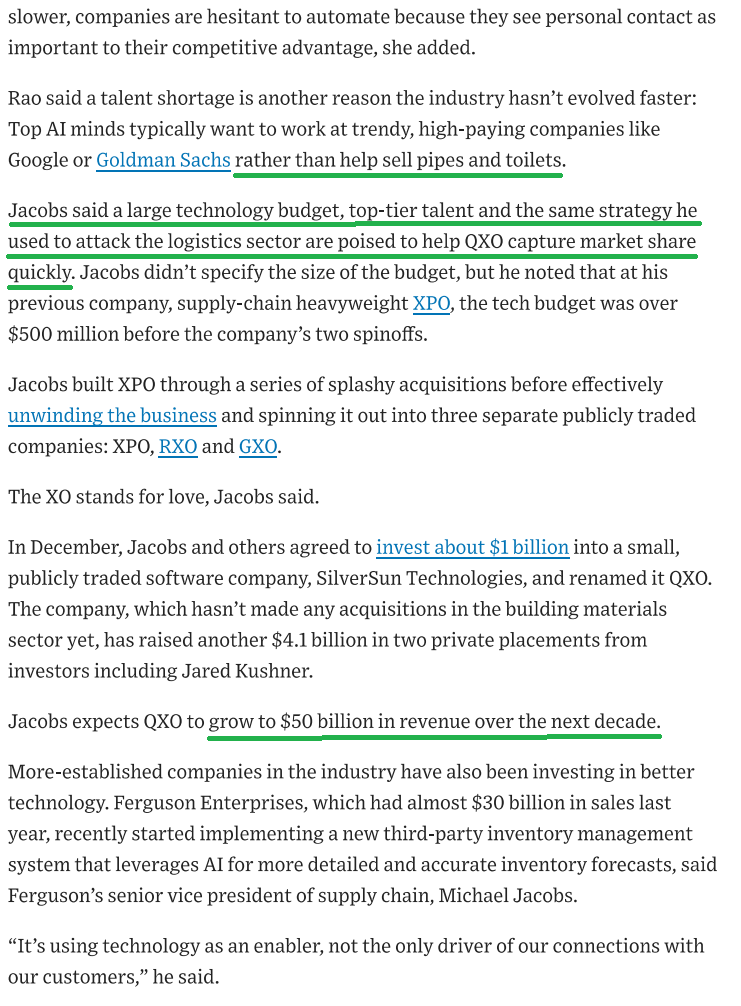

If there’s one takeaway from that interview, it’s that this deal isn’t Brad Jacobs’ first rodeo. In fact, he’s done north of 500. He’s built five companies from scratch, each growing into a billion-dollar or multi-billion-dollar enterprise.

No matter the industry, whether it’s waste management, logistics, or building supply distribution, he runs the same playbook every time. He finds “boring,” fragmented industries with strong fundamentals and outdated operations, ripe for consolidation and automation.

Take United Waste Systems. His strategy was simple: acquire hundreds of small, rural waste collection companies, integrate overlapping routes, streamline operations, and build an efficiently run juggernaut. He then sold the business to what is now Waste Management for $2.2 billion.

At XPO Logistics, it was the same story. He rolled up smaller players in a fragmented market and transformed the industry with technology and automation.

Rinse. Repeat.

After looking over 55 different industries for his next idea, Jacobs landed on building distribution. And just like that, QXO was born.

The industry is as fragmented as they come, with over 7,000 players in North America and 13,000 across Europe. The real kicker is that it’s still mostly run the old-school way: pen and paper, fax machines, and phone orders. Ecommerce only makes up a single to mid-single-digit percentage of total industry revenue. By 2030, that’s expected to triple. And if history tells us anything, we can expect Brad Jacobs to speed up that transformation.

Whether it’s demand forecasting, inventory management, dynamic pricing, or fleet optimization, Brad Jacobs will whip this outdated industry into QXO-like shape—just as he’s done with every company before.

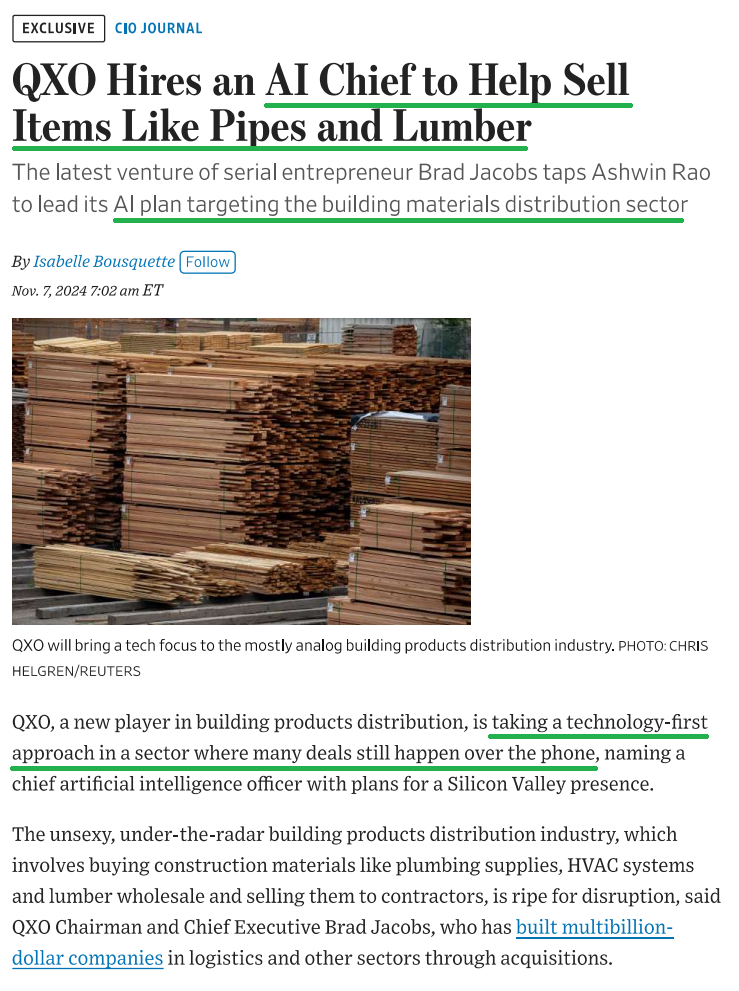

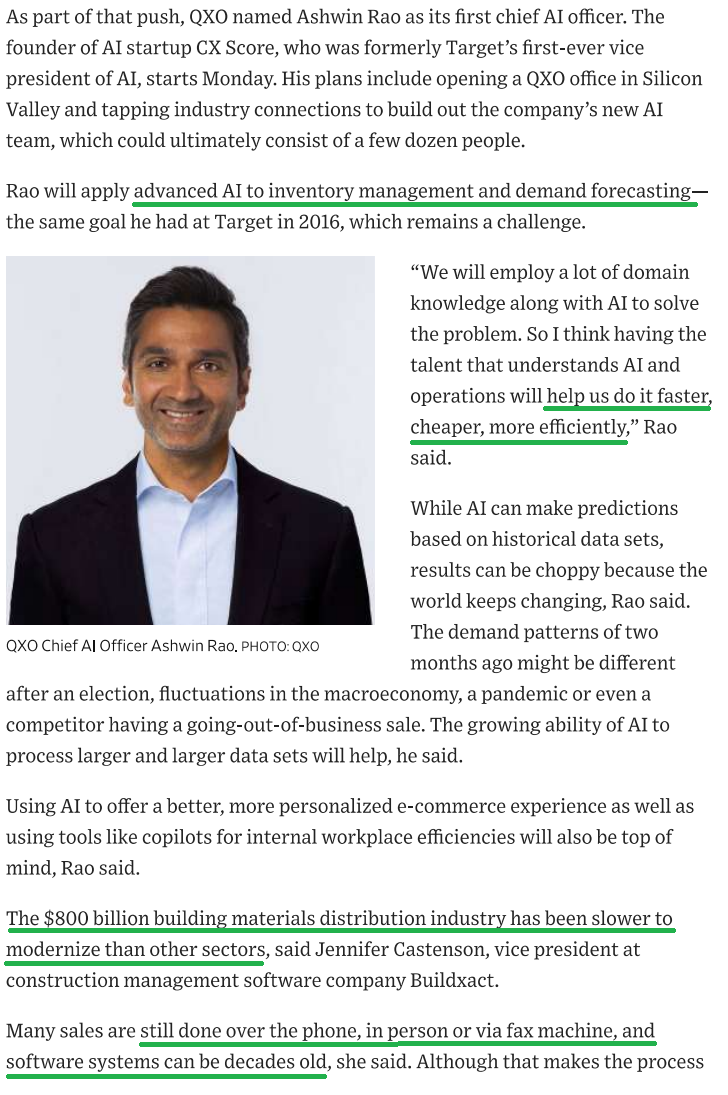

To accelerate the process, QXO has Ashwin Rao, its first Chief AI Officer and the mastermind behind Target’s automated inventory management and demand forecasting, leading the charge.

There are three secular trends that QXO is set to take advantage of:

-

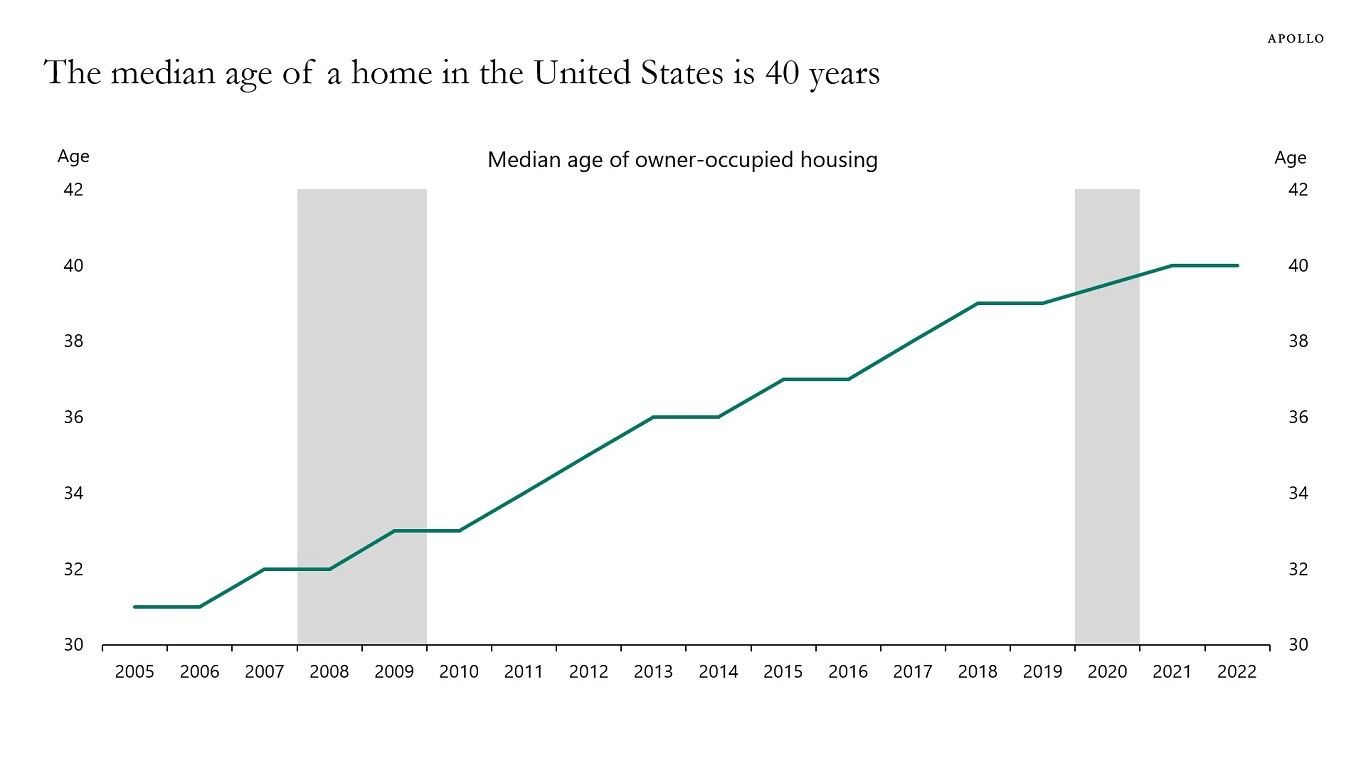

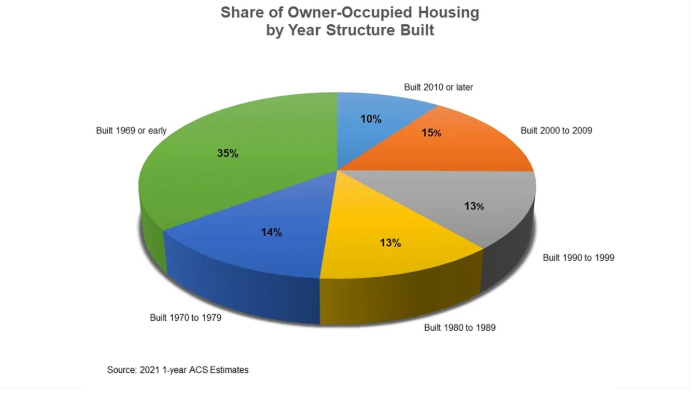

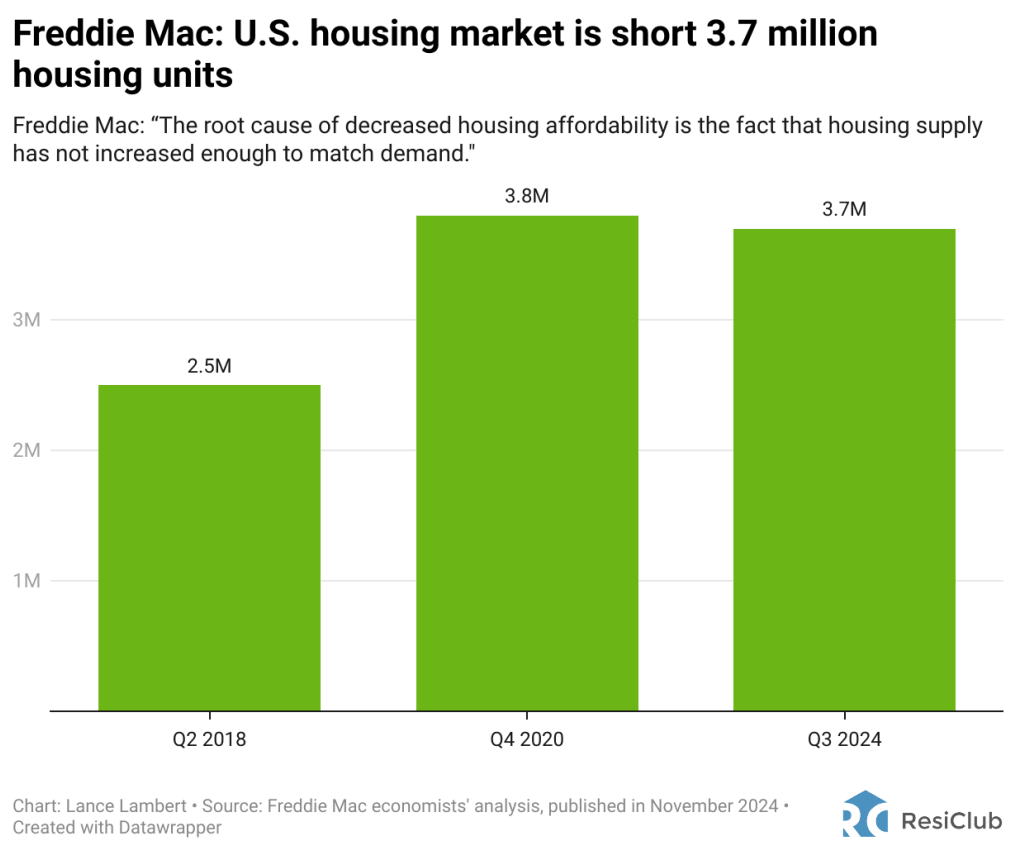

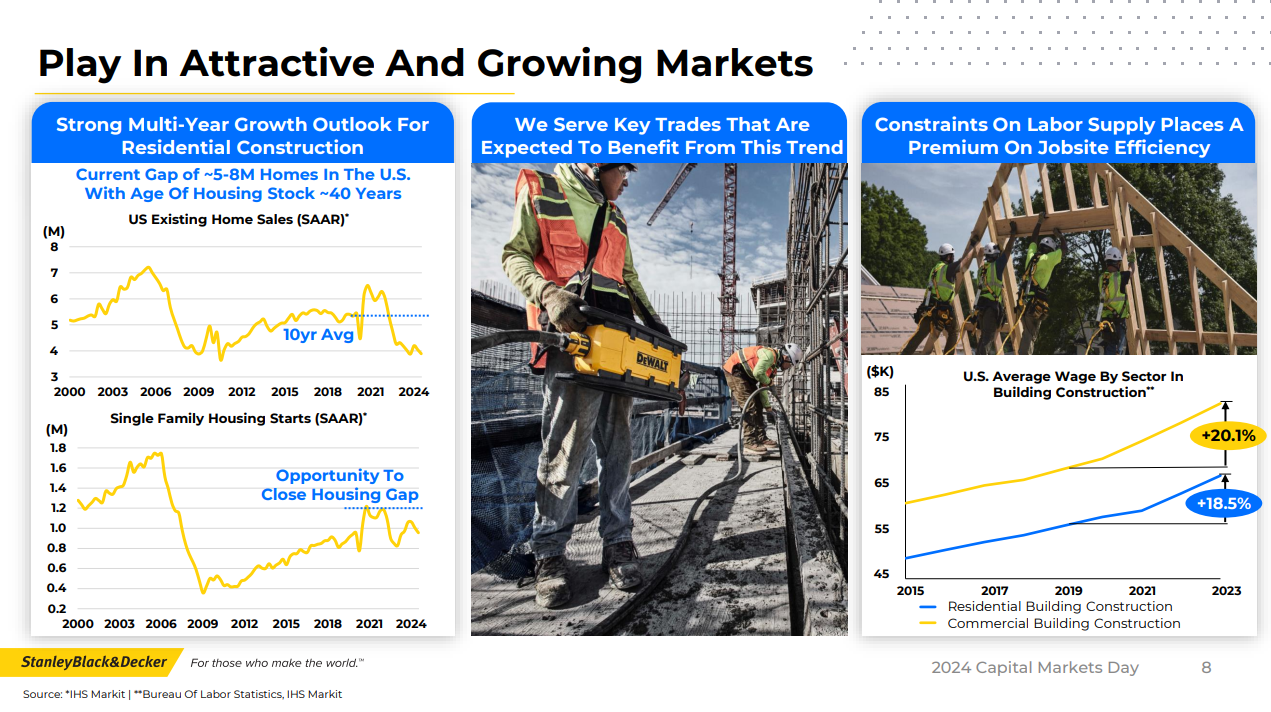

Aging U.S. Residential Homes and the Housing Shortage

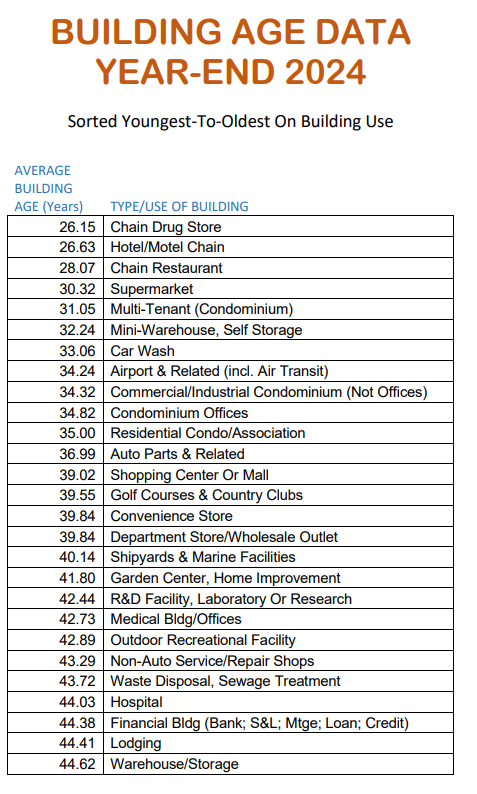

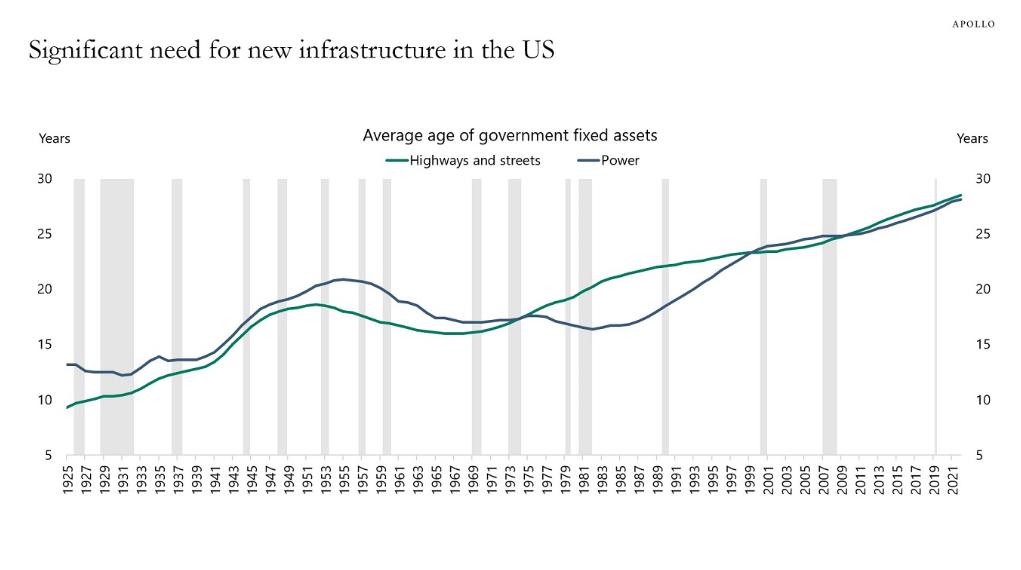

2. Record-high age of U.S. commercial buildings, now averaging ~55 years

3. Over $2 trillion needed for new infrastructure and repairs in the U.S.

These themes and trends should be ringing a bell, reminding us of two of our other favorite levered arms dealer plays on the U.S. housing market recovery: Generac and Stanley Black & Decker.

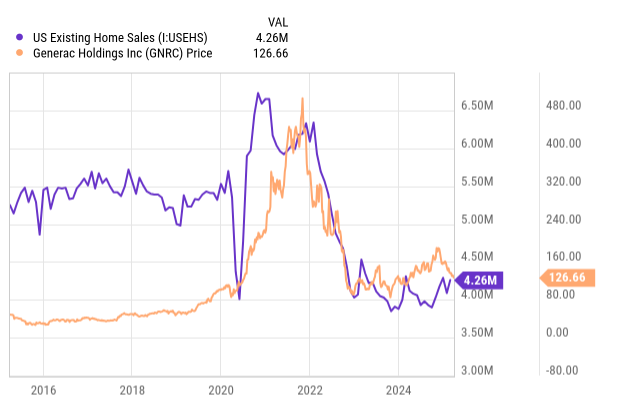

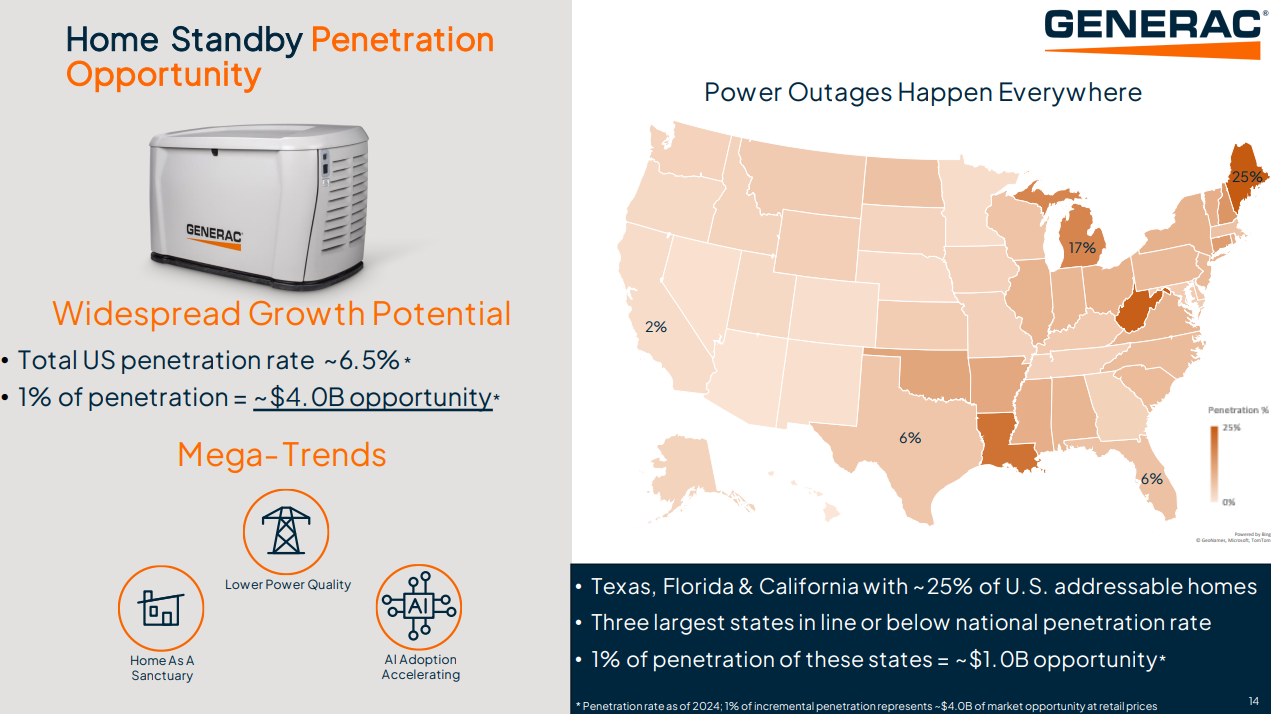

Generac has a total penetration rate of around 6.5% (and growing) in the U.S., with each 1% uptick representing a $4 billion opportunity. If the current administration moves forward with new home construction to address the ~4 million unit housing shortage on federal lands (discussed in detail last week), not only will people get a front-row seat to endangered wildlife in their backyard, but they’ll also likely be purchasing around 260,000 Generac generators for some much-needed backup power.

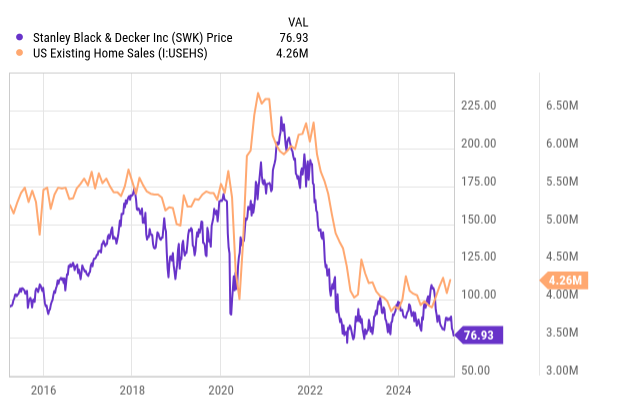

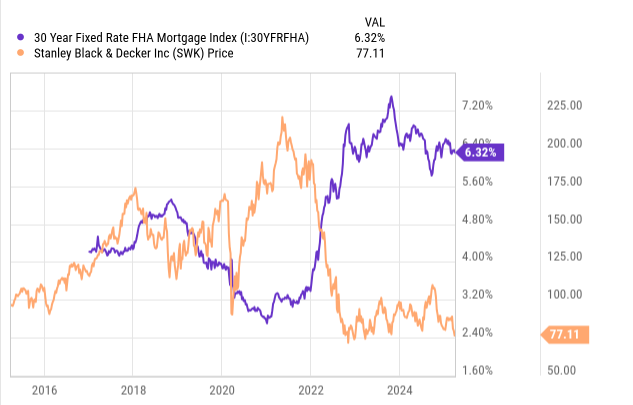

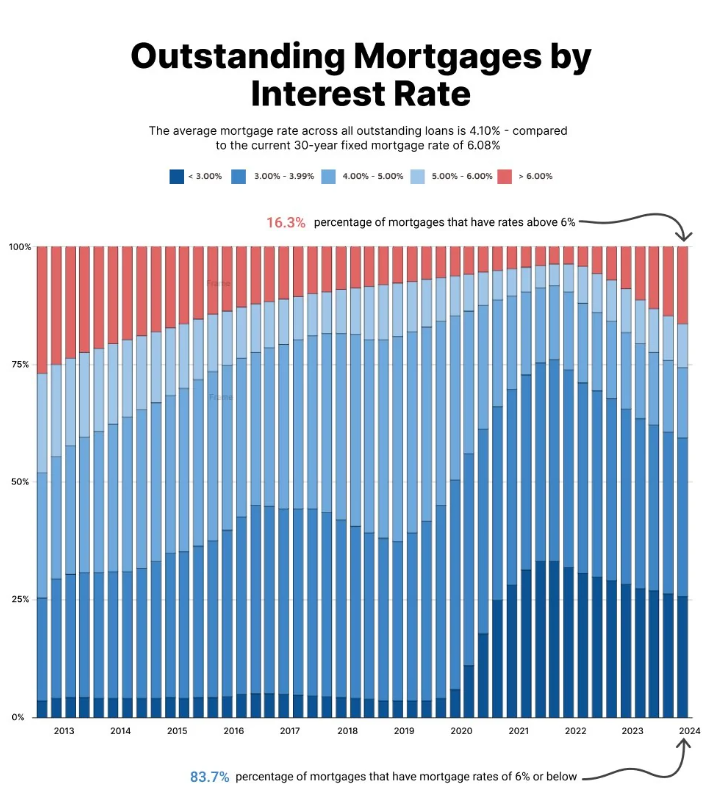

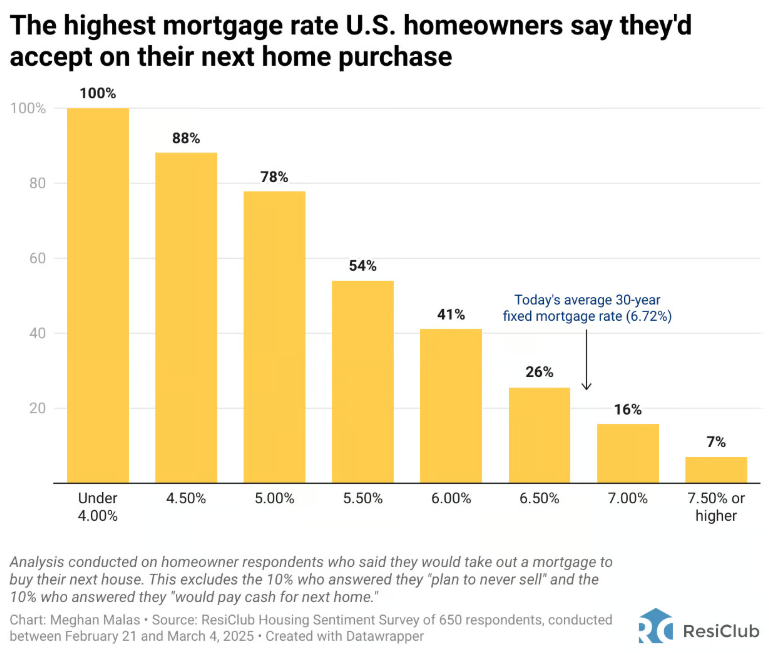

For both SWK and GNRC, the charts are nearly identical. It’s all about re-accelerating existing home sales, which are currently at their lowest annual sales level since 1995.

With over 60% of active mortgages below 4% and the current 30-year fixed rate hovering around 6.65%, the weakness makes sense. But trees don’t grow to the sky, and these things play out in cycles. Always have, always will.

Getting mortgage rates with a 5-handle seems to be the magic number for folks. That’s why bringing down the 10-year yield is by far the most important factor, and luckily, this administration is well aware of it.

Opinion is starting to follow trend:

Scott Bessent went on the “All In” Podcast a few weeks back and shared his playbook for doing just that. I highly recommend giving it a listen:

General Market

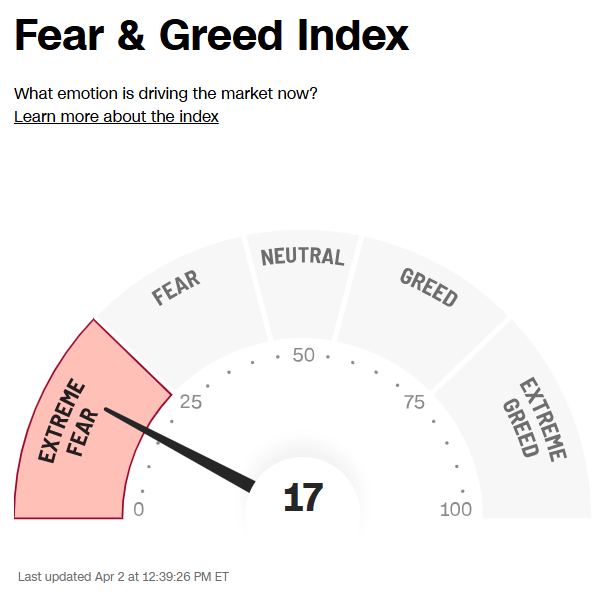

The CNN “Fear and Greed Index” ticked down from 29 last week to 17 this week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

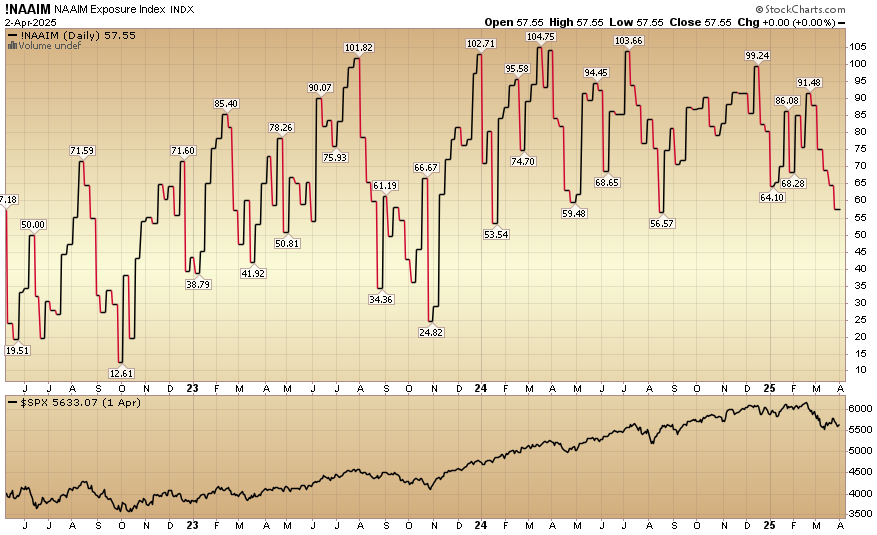

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) ticked down to 57.55% this week from 64.64% equity exposure last week.

Our podcast|videocast will be out sometime on Thursday or Friday. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Congratulations to all of the new clients that came in during our 2024 and Q1 2025 raises. We recently announced our Q2 opening to new clients – for smaller accounts ($1M+). We will be closing our Q2 2025 opening on April 12.

To see if you qualify and to take advantage of this opening click here. Larger accounts $5-10M+ can access bespoke service at their preference here.

*Opinion, Not Advice. See Terms